3. Lesson Plans from the Great Depression: The Banking Crisis (1929–1933)

- Historical Conquest Team

- Jun 22

- 28 min read

How Banks Worked Before the Crisis

Before Americans could understand why thousands of banks failed during the Great Depression, they first needed to understand how banks worked. During the 1920s, banks were at the center of everyday life. Families deposited their paychecks, businesses borrowed money to grow, farmers took out loans to buy equipment, and communities depended on banks to keep money moving through the economy. For millions of Americans, banks seemed as reliable and permanent as schools, churches, and city halls.

A Safe Place for Savings

Most people did not keep large amounts of money at home. Instead, they placed their savings into bank accounts where their money would be protected from theft and could earn interest over time. Savings accounts encouraged families to set money aside for emergencies, future purchases, or retirement. As the economy boomed during the Roaring Twenties, more Americans opened accounts and trusted banks with their hard-earned savings.

Checking Accounts and Everyday Transactions

Banks also provided checking accounts, which allowed customers to write checks instead of carrying large amounts of cash. Businesses used checks to pay suppliers and workers, while families used them to pay bills and make purchases. This system made commerce faster and safer. By helping money move efficiently between individuals and businesses, banks became an essential part of modern economic life.

How Banks Made Money

Many people believed their deposited money simply sat inside a bank vault, but that was not how banking worked. Banks kept only a portion of deposits on hand and loaned the rest to borrowers. They charged interest on these loans and used that income to operate their businesses. As long as only a small number of customers withdrew money at any one time, the system worked smoothly and allowed banks to support economic growth.

Loans That Built America

The money deposited by ordinary citizens helped finance homes, farms, factories, stores, and automobiles. A farmer might borrow money to purchase new equipment. A business owner could borrow funds to expand operations and hire workers. Families often relied on loans to buy homes or make major purchases. Banks acted as financial bridges, connecting people who had money to save with those who needed money to invest.

The Trust That Held Everything Together

The entire banking system depended on one important thing: trust. Depositors trusted that their money would be available when needed, while banks trusted that borrowers would repay their loans. As long as confidence remained strong, the system functioned effectively. However, if people began to fear that banks might fail, they could rush to withdraw their money all at once. Understanding this fragile balance helps explain why the banking crisis of the early 1930s became one of the most devastating events of the Great Depression and why bank failures affected nearly every American family.

Weaknesses Hidden Beneath the Prosperity

During the Roaring Twenties, the United States appeared stronger and wealthier than ever before. Factories produced record numbers of goods, stock prices climbed higher each year, and many Americans believed prosperity would continue forever. Yet beneath the excitement and optimism, serious weaknesses were developing inside the nation's banking system. While newspapers celebrated economic success, many banks were taking risks that would later contribute to one of the greatest financial disasters in American history.

Risky Loans and Easy Credit

Many banks eagerly loaned money to businesses, farmers, and consumers during the 1920s. Easy credit encouraged Americans to buy automobiles, appliances, and other products even when they could not fully afford them. Some banks lowered lending standards because the economy seemed strong and loan repayments appeared certain. As long as businesses prospered and workers remained employed, these loans generated profits. However, if economic conditions changed, many borrowers would struggle to repay their debts, placing banks in danger.

The Stock Market Temptation

The booming stock market attracted not only investors but also banks. Some banks invested depositors' money directly in stocks or loaned large sums to speculators who purchased stocks on margin. These loans depended on stock prices continuing to rise. When prices increased, everyone seemed to benefit. Yet this strategy tied the health of many banks to the fortunes of the stock market. If stock values fell sharply, both investors and banks could suffer enormous losses.

Limited Regulation and Oversight

Banking regulations in the 1920s were far less strict than they would become later. Many small banks operated with little oversight, and there was no federal insurance protecting customer deposits. Bank managers often had wide freedom to make investment and lending decisions. Some were careful and responsible, but others took unnecessary risks. Without strong safeguards, mistakes made by individual banks could quickly become serious problems for entire communities.

Dependence on a Strong Economy

The prosperity of the 1920s hid another major weakness: many banks depended on the economy remaining strong. Businesses needed customers, farmers needed profitable crop prices, and workers needed steady jobs. If any part of this system weakened, loan repayments could slow and bank profits could decline. The banking system was built on confidence and growth, making it far more fragile than many Americans realized.

A Foundation Ready to Crack

By the end of the decade, thousands of banks appeared successful on the surface, but many were already vulnerable. Risky loans, stock market exposure, weak regulations, and dependence on continued prosperity had created hidden cracks beneath the nation's financial foundation. When the economy finally began to falter in 1929, these weaknesses quickly emerged, helping transform a stock market crash into a nationwide banking crisis that would affect millions of Americans.

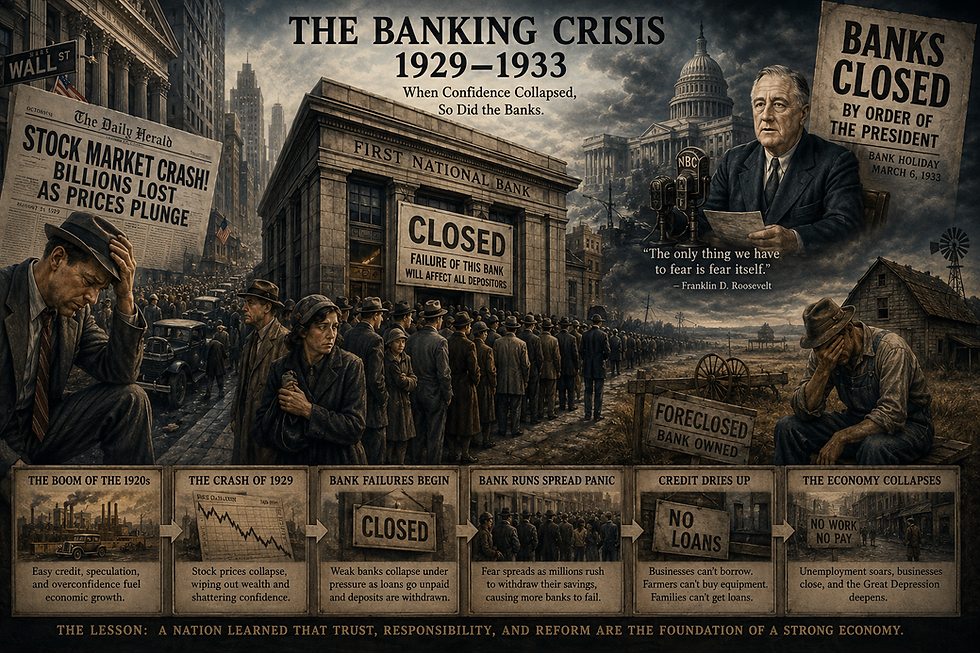

The Stock Market Crash and Its Impact on Banks

When stock prices began collapsing in October 1929, many Americans believed the damage would be limited to investors on Wall Street. Instead, the crash sent shockwaves through the nation's banking system. Banks were deeply connected to the stock market through investments and loans, and as stock values disappeared, financial institutions across the country suddenly found themselves facing serious losses. What began as a stock market disaster quickly became a banking crisis that threatened the savings of millions of Americans.

Banks and the Boom Years

During the prosperous 1920s, many banks benefited from the excitement surrounding the stock market. Some banks invested directly in stocks, hoping to earn large profits as prices climbed higher. Others loaned money to investors who purchased stocks on margin, meaning they borrowed much of the money needed to buy shares. As long as stock prices continued rising, these activities seemed profitable and safe. Few people imagined how quickly conditions could change.

When Prices Came Crashing Down

The stock market's dramatic decline in late 1929 wiped out billions of dollars in paper wealth. Investors who had borrowed money to buy stocks often could not repay their loans once their investments lost value. At the same time, banks that held stocks as assets saw those investments shrink dramatically. Losses spread through the financial system as banks discovered that many of the loans they expected to be repaid were now at risk.

Growing Financial Pressure

As the economy weakened, businesses earned less money and workers lost jobs, making it harder for borrowers to repay loans. Banks faced a growing problem: they had less income coming in while their losses continued to increase. Many institutions found themselves struggling to maintain enough cash reserves to meet customer withdrawals. The financial pressure that followed the crash exposed weaknesses that had been hidden during the years of prosperity.

The Loss of Public Confidence

News of banking troubles spread quickly. Many depositors feared that their banks might fail and rushed to withdraw their savings before it was too late. Even banks that were relatively healthy faced difficulties when large numbers of customers demanded cash at the same time. Fear became almost as dangerous as the financial losses themselves, creating a cycle that pushed many banks closer to collapse.

A Crisis Beyond Wall Street

The stock market crash did far more than reduce stock prices. It weakened banks, disrupted lending, damaged public confidence, and helped turn an economic downturn into a nationwide financial crisis. By exposing the risks banks had taken during the boom years, the crash revealed how closely the fortunes of Wall Street and Main Street had become connected. The problems that began in the stock market would soon spread to communities across the United States, setting the stage for the banking failures that followed.

Bank Runs: When Fear Became a Financial Disaster

During the early years of the Great Depression, one of the most dangerous threats to the banking system was not always a lack of money—it was fear. As news spread of bank failures across the country, millions of Americans began to worry about the safety of their savings. This fear led to bank runs, a phenomenon in which large numbers of depositors rushed to withdraw their money at the same time. What began as concern in one community could quickly become a financial disaster that spread from bank to bank.

Why People Rushed to the Banks

Most Americans trusted banks with their savings, but that trust began to disappear as economic conditions worsened. When people heard rumors that a bank was struggling, they often feared that if they waited too long, they might lose everything. Families, business owners, and workers hurried to their local banks to withdraw cash. Long lines sometimes formed before banks even opened, as anxious customers hoped to secure their savings before it was too late.

How Banking Was Designed to Work

Bank runs were especially dangerous because banks did not keep all deposited money sitting in their vaults. Instead, much of that money had been loaned to businesses, farmers, and homeowners. Under normal circumstances, only a small percentage of customers withdrew money on any given day. This system allowed banks to support economic growth while keeping enough cash available for routine transactions. The system worked well as long as public confidence remained strong.

When Even Healthy Banks Were Threatened

A bank did not have to be poorly managed to experience a bank run. Even a healthy bank with valuable assets could face collapse if too many depositors demanded cash at the same time. Because loans could not be collected immediately and investments could not always be sold quickly, banks often lacked enough cash to satisfy a sudden wave of withdrawals. As a result, institutions that might have survived under normal conditions sometimes failed simply because fear spread faster than confidence.

A Chain Reaction of Panic

Each bank failure created new fear, and each new fear encouraged more withdrawals. Depositors who saw one bank close often worried that their own bank might be next. This created a cycle of panic that spread through towns, cities, and entire states. The more people rushed to withdraw their savings, the more pressure banks faced. In many cases, fear itself became the force that caused the very failures people were trying to avoid.

The Human Cost of Panic

Bank runs devastated countless families. When banks closed their doors, depositors often lost access to money they had spent years saving. Businesses struggled to pay workers, farmers lost operating funds, and communities faced growing uncertainty. The wave of bank runs during the Great Depression demonstrated that financial systems depend not only on money and investments but also on public trust. Once that trust disappeared, the consequences could be felt throughout the entire nation.

Why Thousands of Banks Failed

Between 1930 and 1933, the United States experienced one of the worst banking disasters in its history. More than 9,000 banks closed their doors during the Great Depression, wiping out savings, disrupting businesses, and shaking public confidence in the financial system. These failures did not happen because of a single event. Instead, a combination of economic problems, poor decisions, and growing panic created a chain reaction that overwhelmed thousands of financial institutions across the country.

Poor Investments During the Boom Years

Many banks entered the Depression carrying risks they had taken during the prosperous 1920s. Some had invested heavily in stocks, real estate, or speculative ventures that seemed profitable when the economy was growing. When the stock market crashed and property values declined, these investments lost much of their value. Banks that had counted on these assets to remain strong suddenly faced major financial losses.

Loans That Were Never Repaid

Banks earned money by lending funds to farmers, businesses, and consumers. As the Depression deepened, many borrowers found themselves unable to repay what they owed. Businesses closed, workers lost jobs, and families struggled to make ends meet. Every unpaid loan weakened a bank's financial position. As more borrowers defaulted, many institutions found themselves with fewer resources available to meet their obligations.

The Crisis in Farm Country

Rural banks faced especially difficult challenges. Agricultural prices had been falling since the end of World War I, and many farmers were already struggling before the Depression began. As crop prices dropped even further, farmers earned less money and had trouble repaying loans. Because many small-town banks depended heavily on agricultural customers, the hardships faced by farmers quickly became hardships for their local banks as well.

A Shrinking Economy

The banking crisis worsened as business activity declined across the nation. Factories reduced production, stores sold fewer goods, and companies postponed expansion plans. Fewer business transactions meant fewer opportunities for banks to earn profits. At the same time, declining property values and falling incomes reduced the value of many assets held by financial institutions. The shrinking economy placed pressure on banks from nearly every direction.

Panic Among Depositors

Perhaps the most powerful force behind many bank failures was fear itself. As people heard reports of banks closing, they rushed to withdraw their savings before their own institutions might fail. These bank runs drained cash reserves and placed enormous pressure on banks. Even institutions that might have survived under normal conditions often collapsed when large numbers of depositors demanded their money at the same time.

The Collapse of Confidence

By early 1933, the banking system faced a crisis of confidence unlike anything the nation had experienced before. Thousands of banks had failed, millions of Americans had lost savings, and trust in financial institutions had nearly vanished. The wave of failures demonstrated how closely banks depended on both economic stability and public confidence. When those foundations cracked, the result was a banking disaster that deepened the Great Depression and changed the American financial system forever.

Families Who Lost Their Savings

For many Americans, the banking crisis was not just a financial event reported in newspapers—it was a personal tragedy that changed their lives forever. When banks failed during the Great Depression, millions of people suddenly lost access to the money they had worked for, saved, and trusted banks to protect. Families who had carefully planned for the future found themselves facing uncertainty almost overnight. The collapse of banks transformed an economic crisis into a deeply human one.

A Lifetime of Savings Gone

Many Americans spent years setting aside small amounts of money from each paycheck. They believed their savings were secure in local banks. When those banks closed, however, depositors often could not withdraw their funds. Some eventually recovered a portion of their money, but others lost much of what they had saved. For families who had spent decades building financial security, the shock was devastating.

Workers Facing New Hardships

Factory workers, miners, teachers, and laborers depended on their savings to survive difficult times. When banks failed, many workers lost emergency funds they had hoped would protect them from unemployment or illness. As jobs became scarce during the Depression, access to savings became even more important. Without those funds, many families struggled to buy food, pay rent, or cover basic household expenses.

Retirees Without a Safety Net

Older Americans were among the hardest hit. Before modern retirement programs became widespread, many retirees relied heavily on personal savings. A bank failure could erase years of careful planning. Elderly citizens who expected to spend their later years in comfort often found themselves dependent on relatives, charities, or community assistance. For many, the loss of savings meant losing their independence as well.

Small Business Owners in Trouble

Local shopkeepers, restaurant owners, and other small business operators often kept business funds in banks. When those deposits became unavailable, it became difficult to pay employees, purchase inventory, or cover monthly expenses. Some businesses that had survived the economic downturn were pushed into bankruptcy simply because they could no longer access their own money. Entire communities felt the effects as local businesses struggled or closed their doors.

Communities Changed Forever

The impact of bank failures extended beyond individual families. Neighbors helped one another, churches organized relief efforts, and local charities worked to assist those in need. Yet the loss of savings weakened communities and damaged trust in financial institutions. People who had once viewed banks as symbols of security now worried about where to keep their money. The experience left lasting memories that shaped attitudes toward banking for generations.

The Human Face of the Banking Crisis

Behind every bank failure was a story of real people whose lives were disrupted by events beyond their control. Families lost nest eggs, workers lost security, retirees lost independence, and business owners lost opportunities. The banking crisis of the Great Depression reminds us that financial systems affect more than numbers on paper—they affect the hopes, dreams, and futures of millions of people who depend on them every day.

The Collapse of Credit

When thousands of banks failed during the Great Depression, Americans lost more than savings accounts and financial security. They also lost access to credit, the borrowed money that helped businesses expand, farmers operate, and families make important purchases. Credit had fueled much of the economic growth of the 1920s, but as banks disappeared and confidence collapsed, loans became increasingly difficult to obtain. The result was a credit crisis that deepened the Great Depression and slowed economic recovery across the nation.

Why Credit Matters

Credit plays a vital role in a modern economy. Businesses use loans to purchase equipment, build new facilities, and hire workers. Farmers often borrow money to buy seed, livestock, machinery, and land. Families rely on loans to purchase homes, automobiles, and other major necessities. When banks are willing to lend, money flows through the economy, creating opportunities for growth and investment. When lending stops, economic activity slows dramatically.

Banks Stop Making Loans

As banks experienced losses and faced growing uncertainty, many became reluctant to lend money. Some institutions failed entirely, while others tightened lending standards to protect their remaining funds. Bank managers worried that new borrowers might not be able to repay their debts in a struggling economy. As a result, even qualified individuals and businesses often found it difficult to obtain the financing they needed.

Businesses Struggle to Survive

Without access to credit, many businesses could not expand or even maintain normal operations. Companies delayed purchases of machinery, postponed construction projects, and reduced hiring. Some businesses that might have survived the economic downturn were forced to close because they could not secure short-term loans to cover expenses. As businesses failed, unemployment increased, reducing consumer spending and creating even more economic hardship.

Farmers Face Growing Challenges

American farmers were especially vulnerable to the collapse of credit. Many depended on seasonal loans to plant crops and purchase supplies before harvest time. With banks unwilling or unable to lend, farmers struggled to buy seed, fertilizer, and equipment. Falling crop prices made matters worse, leaving many unable to repay existing debts. The agricultural sector, already weakened during the 1920s, suffered even greater losses during the Depression.

Consumers Put Life on Hold

Ordinary Americans also felt the effects of the credit crisis. Families postponed buying homes, automobiles, and household goods because loans were unavailable or difficult to obtain. As consumer spending declined, factories produced fewer products and stores sold less merchandise. This reduction in demand contributed to additional layoffs and business failures, spreading the effects of the Depression throughout the economy.

A Downward Economic Spiral

The collapse of credit created a powerful chain reaction. Bank failures reduced lending, reduced lending slowed business activity, and slower business activity led to more unemployment and financial losses. Each problem strengthened the next, creating a downward spiral that deepened the Great Depression. The credit crisis demonstrated how important banks were to the functioning of the economy and how the loss of lending could turn a severe downturn into a prolonged national disaster.

Rural Banks and the Agricultural Crisis

While the banking crisis affected Americans across the nation, some of the hardest-hit communities were found far from the nation's cities and financial centers. In farming regions, local banks and local farmers depended heavily upon one another for survival. When agricultural prices collapsed and farmers struggled to repay loans, many rural banks found themselves facing a financial disaster. Long before some urban banks encountered serious trouble, farming communities were already experiencing the painful effects of economic decline.

The Close Connection Between Farms and Banks

Rural banks served as the financial backbone of agricultural communities. Farmers borrowed money to purchase land, livestock, tractors, seed, and other supplies needed for planting and harvesting. In return, banks depended on farmers to repay those loans after successful growing seasons. As long as crop prices remained strong and harvests were profitable, this relationship benefited both farmers and banks.

Falling Crop Prices Create Trouble

After World War I, American farmers faced growing challenges. During the war, high demand for food had encouraged farmers to expand production and borrow money for additional land and equipment. When the war ended, demand declined and crop prices began to fall. By the late 1920s and early 1930s, many farmers were earning far less for their wheat, corn, cotton, and other crops than they had expected. Lower prices meant lower incomes, making it difficult to repay loans.

When Farmers Could Not Pay

As farm incomes declined, loan payments became harder to make. Some farmers missed payments, while others defaulted entirely. Because rural banks often held large numbers of agricultural loans, even a modest increase in unpaid debts could create serious financial problems. The more farmers struggled, the more pressure local banks faced. In many communities, the fortunes of the bank rose and fell alongside the fortunes of the farms it served.

The Failure of Small-Town Banks

Many rural banks were small institutions with limited resources. Unlike larger city banks, they often lacked diversified investments and depended heavily on the success of local agriculture. When farm loans went unpaid and depositors became concerned about the bank's future, some institutions quickly ran out of money. Hundreds of rural banks closed their doors, leaving communities without an important source of financial support.

Communities Under Strain

The collapse of rural banks created difficulties that extended beyond individual farmers. Local businesses lost customers, workers lost jobs, and entire towns suffered economic decline. Without functioning banks, obtaining credit became extremely difficult, making recovery even harder. Families who had trusted their savings to local institutions often found themselves facing financial uncertainty alongside their struggling neighbors.

A Warning Before the National Crisis

The troubles faced by rural banks provided an early warning of the larger banking crisis that would soon spread across the nation. Falling crop prices, unpaid loans, and shrinking economic activity exposed weaknesses in the financial system years before the worst bank failures occurred. The experience of farming communities demonstrated how closely banks were tied to the health of the economy and how problems in one sector could spread throughout the entire nation.

The Banking Panic of 1933

By early 1933, the American banking system stood on the edge of collapse. For more than three years, bank failures, economic hardship, and public fear had spread across the nation. Millions of Americans worried that their savings could disappear at any moment. As confidence vanished and panic intensified, the country entered the final and most dangerous stage of the banking crisis. Many feared that if immediate action was not taken, the entire financial system might fail.

A Nation Losing Confidence

Throughout the Great Depression, thousands of banks had already closed their doors. Each failure caused new anxiety among depositors. People read newspaper reports of failing banks, heard stories from friends and relatives, and wondered whether their own savings were safe. By 1933, confidence in the banking system had become dangerously weak. Fear was spreading faster than banks could reassure their customers.

The Rush to Withdraw Money

As panic grew, depositors across the country rushed to withdraw their money. Long lines formed outside banks as people demanded cash before it was too late. Even financially stable banks struggled under the pressure because banks did not keep enough cash on hand to satisfy every depositor at once. The more people withdrew their money, the more vulnerable banks became, creating a cycle that fed on fear itself.

State Bank Holidays

Facing growing panic, several state governors took extraordinary action. They declared temporary "bank holidays," ordering banks to close for short periods to stop the flow of withdrawals. These closures were designed to prevent banks from running out of cash and to give officials time to assess the financial condition of local institutions. While intended as emergency measures, the closures also revealed just how serious the crisis had become.

Emergency Closures Across the Nation

As conditions worsened, banking restrictions spread from state to state. Businesses struggled to conduct transactions, workers worried about receiving wages, and families wondered whether they would regain access to their savings. The financial system that Americans depended upon for daily life was becoming increasingly unstable. By March 1933, many communities were operating under emergency banking restrictions unlike anything seen before in American history.

Fear of Total Collapse

The greatest concern was that the panic would continue until no bank could survive. If every depositor demanded cash at the same time, even strong banks would be unable to meet those requests immediately. Economists, government officials, business leaders, and ordinary citizens feared that the nation's entire banking structure might collapse. Such an event would have crippled trade, destroyed savings, and made economic recovery far more difficult.

The Crisis Reaches Its Peak

The Banking Panic of 1933 marked the high point of the nation's banking emergency. Years of failures, unpaid loans, declining business activity, and public fear had pushed the financial system to its breaking point. Although dramatic actions would soon be taken to restore confidence, the panic demonstrated how essential trust was to banking. Without confidence, even the strongest financial institutions could be threatened, making the crisis one of the most dramatic moments of the Great Depression.

Lessons Learned and the Rebuilding of Trust

By 1933, the United States had endured years of bank failures, lost savings, business closures, and widespread uncertainty. Millions of Americans had seen how quickly confidence in the financial system could disappear and how deeply that loss of trust could affect everyday life. As the banking crisis began to stabilize, citizens, bankers, and government leaders looked back at the painful lessons of the Great Depression and searched for ways to build a stronger and more reliable financial system for the future.

The Importance of Trust

One of the clearest lessons of the banking crisis was that trust is the foundation of banking. Banks depend on depositors believing their money will be safe and available when needed. When confidence vanished, people rushed to withdraw their savings, creating bank runs that damaged even healthy institutions. Americans learned that a financial system could not function properly without public trust and confidence.

The Need for Responsible Lending

The crisis also revealed the dangers of excessive risk-taking. During the prosperous years of the 1920s, some banks made risky loans and investments while assuming economic growth would continue indefinitely. When conditions changed, many borrowers could not repay their debts, and financial losses spread throughout the banking system. The experience demonstrated the importance of careful lending practices and sound financial decision-making.

The Role of Financial Oversight

Another lesson involved the need for stronger oversight of financial institutions. Before the Great Depression, many banks operated with limited supervision and few protections for depositors. The crisis showed that weaknesses in one part of the financial system could quickly affect communities across the nation. Americans increasingly recognized that oversight could help identify problems before they became nationwide emergencies.

Protecting Depositors

Perhaps the most personal lesson involved protecting ordinary citizens. Families who had spent years saving money often lost access to their funds when banks failed. Workers, retirees, and small business owners discovered how vulnerable they were when financial institutions collapsed. As the nation recovered, protecting depositors became an important goal in efforts to restore confidence and encourage people to trust banks once again.

A Stronger Foundation for the Future

The banking crisis transformed the way many Americans thought about money, savings, and financial institutions. It demonstrated that prosperity alone could not guarantee stability and that strong financial systems required responsibility, transparency, and public confidence. The lessons learned from the crisis helped shape future reforms and recovery efforts, creating a bridge to the next stage of the Great Depression as leaders sought solutions to rebuild the economy and restore hope to a struggling nation.

Remembering the Lessons

The story of the banking crisis is not only a story about money—it is a story about trust, responsibility, and resilience. The hardships endured by millions of Americans taught valuable lessons about the importance of protecting savings, maintaining confidence in financial institutions, and preparing for economic challenges. Those lessons would influence the nation's recovery and continue shaping American banking for generations to come.

World Events That Influenced the Banking Crisis (1929–1933)

Germany's Economic Collapse (1930–1932)

Germany suffered particularly severe economic hardship during the early years of the Great Depression. German banks faced growing losses, businesses failed, and unemployment soared. In 1931, several major German financial institutions collapsed or required emergency assistance. Because American banks and investors had provided loans to Germany during the 1920s, Germany's financial troubles created concerns among American bankers and investors. The instability of one of Europe's largest economies further weakened confidence in the international banking system.

The Austrian Banking Crisis of 1931

One of the most important international financial events occurred in May 1931 when Austria's largest bank, Creditanstalt, announced massive losses and nearly collapsed. The crisis shocked investors throughout Europe and the United States. Fear spread rapidly as people worried that other banks might be in similar trouble. The failure damaged confidence in international banking and contributed to a broader wave of financial panic that made conditions worse for American banks already struggling with their own problems.

The Collapse of International Trade

As economies weakened around the world, international trade declined dramatically. Countries imported fewer goods, factories produced less, and shipping activity slowed. American farmers and manufacturers found it harder to sell products overseas, reducing business profits and incomes. Lower earnings made it more difficult for businesses and individuals to repay loans, increasing the financial pressure on banks. The decline of global trade turned what might have been a national crisis into a worldwide economic disaster.

Britain Leaves the Gold Standard (1931)

In September 1931, Britain abandoned the Gold Standard, a system that linked currency values to gold reserves. This decision shocked financial markets around the world because Britain had long been one of the world's leading financial powers. Investors worried that other countries might take similar actions. The uncertainty contributed to international financial instability and increased concerns about the strength of banks and currencies worldwide.

Political Extremism and Social Unrest

The economic hardships of the early 1930s fueled political unrest in many countries. High unemployment, poverty, and frustration with governments led some citizens to support extremist political movements. In Germany, economic instability contributed to the growing popularity of political groups that promised dramatic solutions to national problems. These political uncertainties increased fears among investors and businesses, making economic recovery even more difficult.

Japan's Expansion into Manchuria (1931)

While financial troubles spread, Japan invaded Manchuria in northeastern China in 1931. The invasion increased international tensions and raised concerns about future conflicts. Although the event did not directly cause bank failures in the United States, it contributed to global uncertainty. Businesses and investors were already nervous about economic conditions, and growing international instability further weakened confidence in the future.

A Worldwide Depression

By 1932 and 1933, the Great Depression had become a global crisis affecting nearly every major economy. Banks failed in multiple countries, unemployment reached record levels, and governments struggled to find solutions. Because economies were connected through trade, investments, and debt, problems in one nation often spread to others. The American banking crisis was therefore both a national tragedy and part of a much larger worldwide economic collapse.

The Most Important People During The Banking Crisis (1929–1933)

Herbert Hoover – President During the Crisis

Herbert Hoover served as President of the United States from 1929 to 1933, meaning he was in office when the stock market crashed and much of the banking crisis unfolded. Before becoming president, Hoover had earned an international reputation as an engineer and humanitarian who organized relief efforts during and after World War I. As the crisis deepened, Hoover encouraged voluntary cooperation between businesses and banks and supported some government intervention, but many Americans believed his response was too limited. His presidency became closely associated with the hardships of the early Depression years.

Franklin D. Roosevelt – Restoring Public Confidence

Franklin Roosevelt entered office in March 1933 during the height of the banking panic. One of his first actions was to declare a national Bank Holiday, temporarily closing banks while federal officials examined their financial condition. Through his leadership and public communication, including his famous Fireside Chats, Roosevelt helped restore confidence in the banking system. His administration oversaw reforms that would reshape American banking for generations.

Eugene Meyer – Stabilizing the Financial System

Eugene Meyer served as chairman of the Federal Reserve Board during some of the most difficult years of the crisis. A successful businessman and financier, Meyer worked to strengthen the banking system and support financial recovery. He also played a role in the creation of the Reconstruction Finance Corporation, which provided emergency loans to struggling banks and businesses. Later, he became the owner of the newspaper The Washington Post.

Marriner S. Eccles – A Voice for Reform

Marriner Eccles was a banker from Utah who witnessed the devastation caused by the banking crisis. Unlike many business leaders of his era, he argued that the federal government needed to take stronger action to stimulate the economy and stabilize the financial system. His ideas influenced future banking and economic policies, and he later became one of the most influential leaders of the Federal Reserve System.

Carter Glass – Architect of Banking Reform

Carter Glass had helped create the Federal Reserve System in 1913 and remained one of the nation's leading experts on banking policy during the crisis. As a senator, he advocated reforms designed to strengthen the banking system and restore public confidence. His work contributed to legislation that separated commercial banking from investment banking, helping reduce some of the risks that had contributed to financial instability.

Frances Perkins – Champion for Ordinary Americans

Frances Perkins became the first woman to serve in a presidential cabinet when Roosevelt appointed her Secretary of Labor in 1933. Although not a banker, she played an important role in shaping policies designed to protect workers and families suffering from the effects of the banking crisis and the broader Great Depression. Her advocacy helped influence reforms that improved economic security for millions of Americans.

Charles E. Mitchell – Symbol of the Speculative Era

Charles Mitchell was one of the most powerful bankers of the 1920s and led National City Bank, one of the largest banks in the United States. He became famous for encouraging investment and expansion during the stock market boom. After the crash, critics accused bankers like Mitchell of encouraging excessive speculation and risky financial practices. His career became a symbol of both the opportunities and dangers of the Roaring Twenties financial system.

Life Lessons and Thought Processes from The Banking Crisis (1929–1933)

Prosperity Does Not Last Forever

One of the most important lessons from the banking crisis is that good times do not continue indefinitely. During the Roaring Twenties, many Americans assumed that rising stock prices, growing businesses, and expanding wealth would continue forever. This belief caused some individuals and institutions to take risks they might have avoided during more cautious times. The crisis teaches us to prepare for challenges even when circumstances appear favorable.

Understand the Risks Before Making Decisions

Many banks made risky loans and investments without fully considering what might happen if the economy slowed. When conditions changed, those risks became major problems. This lesson applies to many areas of life. Before making important decisions, it is wise to ask what could go wrong and whether the potential rewards justify the risks involved.

Do Not Let Fear Control Your Actions

The banking crisis demonstrated how fear can spread rapidly through a population. Rumors and panic caused many depositors to rush to banks and withdraw money. In some cases, fear helped create the very failures people were trying to avoid. This teaches the importance of remaining calm during difficult situations, gathering accurate information, and making thoughtful decisions rather than reacting emotionally.

Trust Is Difficult to Build and Easy to Lose

Banks depend on trust. Customers must believe their money is safe, and borrowers must be trusted to repay loans. Once confidence disappeared, restoring it became extremely difficult. This lesson extends beyond banking. Whether in friendships, families, schools, businesses, or governments, trust is one of the most valuable resources people possess. It often takes years to earn but can be lost very quickly.

Small Problems Can Become Large Crises

Many of the issues that contributed to the banking crisis developed gradually over time. Risky loans, weak regulations, and declining farm incomes were warning signs that often went unnoticed or ignored. The crisis teaches us to pay attention to small problems before they grow into larger ones. Addressing challenges early is usually easier than waiting until they become emergencies.

The Importance of Preparation

Families who had emergency savings, businesses that avoided excessive debt, and banks that managed risks carefully often weathered the crisis better than others. Preparation does not eliminate difficulties, but it can reduce their impact. This lesson encourages individuals to think ahead, save resources, and develop plans for unexpected situations.

Vocabulary to Learn While Studying the Banking Crisis after 1929

1. Bank FailureDefinition: The closing of a bank because it does not have enough money or assets to meet its obligations to customers and creditors.Sample Sentence: Thousands of Americans lost access to their savings when a bank failure occurred during the Great Depression.

2. DepositDefinition: Money placed into a bank account for safekeeping.Sample Sentence: Sarah made a deposit into her savings account after receiving her paycheck.

3. WithdrawalDefinition: The act of taking money out of a bank account.Sample Sentence: Many people rushed to make a withdrawal when rumors spread that their local bank was in trouble.

4. Savings AccountDefinition: A bank account designed to hold money and earn interest over time.Sample Sentence: The family kept its emergency fund in a savings account at the local bank.

5. Checking AccountDefinition: A bank account used for everyday spending and writing checks.Sample Sentence: The store owner paid suppliers using funds from a checking account.

6. LoanDefinition: Money borrowed from a bank or lender that must be repaid, usually with interest.Sample Sentence: The farmer obtained a loan to purchase new farming equipment.

7. InterestDefinition: The amount charged for borrowing money or earned for saving money in a bank.Sample Sentence: The bank paid interest on money deposited in savings accounts.

7. CreditDefinition: The ability to borrow money with the promise of repaying it later.Sample Sentence: Many businesses struggled when credit became difficult to obtain during the Depression.

8. CollateralDefinition: Property or valuables pledged to secure a loan.Sample Sentence: The farmer used part of his land as collateral for a bank loan.

9. DefaultDefinition: Failure to repay a loan according to the agreed terms.Sample Sentence: Rising unemployment caused many borrowers to default on their loans.

10. ReserveDefinition: Money that banks keep available to meet customer withdrawals.Sample Sentence: Banks needed sufficient reserves to satisfy customers who wanted their money.

11. LiquidityDefinition: The ability to quickly convert assets into cash.Sample Sentence: A lack of liquidity made it difficult for some banks to survive a bank run.

12. Bank RunDefinition: A situation in which many depositors withdraw their money from a bank at the same time.Sample Sentence: Fear of losing savings triggered a bank run in the small farming town.

13. DepositorDefinition: A person or organization that places money in a bank account.Sample Sentence: Each depositor hoped the bank would remain open during the crisis.

14. AssetDefinition: Anything of value owned by a person, business, or bank.Sample Sentence: Loans and investments were important assets held by many banks.

15. LiabilityDefinition: A debt or financial obligation owed by a person, business, or bank.Sample Sentence: Customer deposits are considered liabilities because banks owe that money to depositors.

16. SolventDefinition: Having enough assets to cover debts and continue operating.Sample Sentence: The bank remained solvent despite economic difficulties.

17. InsolventDefinition: Unable to pay debts because liabilities exceed assets.Sample Sentence: Several institutions became insolvent after suffering heavy investment losses.

18. PanicDefinition: Sudden widespread fear that causes people to act emotionally rather than rationally.Sample Sentence: Financial panic spread across the country as more banks closed.

19. Bank HolidayDefinition: A temporary government-ordered closure of banks to prevent further withdrawals and stabilize the financial system.Sample Sentence: In 1933, a bank holiday was declared to help stop the banking panic.

20. Federal ReserveDefinition: The central banking system of the United States responsible for managing monetary policy and financial stability.Sample Sentence: The Federal Reserve worked to support the banking system during the crisis.

Activities to Try While Studying The Banking Crisis after 1929

The Great Bank Run Simulation

Recommended Age: 10–18

Activity Description: Students participate in a simulation that demonstrates how a bank run occurs. Some students act as bankers, while others act as depositors. The activity shows how even a healthy bank can fail when too many people demand cash at the same time.

Objective: To understand how bank runs occurred and why public confidence was essential to the banking system.

Materials: Play money, envelopes, calculator, role cards, paper for recording transactions.

Instructions:

Choose one student to be the banker and the rest to be depositors.

Give each depositor $100 in play money and have them deposit it into the bank.

Explain that the bank only keeps 20% of deposits on hand and loans out the rest.

Announce that a rumor is spreading that the bank may fail.

Allow depositors to decide whether to withdraw their money.

Count how much cash the bank has available compared to how much depositors want.

Discuss what happened and why.

Learning Outcome: Students will understand how fear and panic contributed to bank failures during the Great Depression.

A Family During the Banking Crisis

Recommended Age: 11–18

Activity Description: Students assume the role of a family living during the early 1930s and must make difficult financial decisions after their bank closes.

Objective: To understand the human impact of bank failures on ordinary Americans.

Materials: Family scenario cards, budgeting worksheet, pencils.

Instructions:

Provide students with a family profile including income, savings, debts, and monthly expenses.

Inform students that their bank has failed and most of their savings are unavailable.

Have students decide which expenses they can pay and which they must postpone.

Ask students to discuss how they would adapt to the situation.

Compare different groups' solutions and challenges.

Learning Outcome: Students will develop empathy for families affected by the banking crisis and understand the difficult choices many Americans faced.

Follow the Money

Recommended Age: 10–16

Activity Description: Students trace the path of money through a community to see how banks support economic activity.

Objective: To understand the role banks play in lending and economic growth.

Materials: String, note cards, play money, name tags.

Instructions:

Assign roles such as farmer, store owner, banker, factory worker, and customer.

Use string to connect participants as money flows through the community.

Introduce a bank failure and remove the bank from the network.

Observe how transactions become more difficult.

Discuss the consequences for each participant.

Learning Outcome: Students will see how bank failures affected entire communities rather than just individual depositors.

Build and Break a Banking System

Recommended Age: 12–18

Activity Description: Students create a simple model banking system and observe how loans, savings, and economic conditions affect its stability.

Objective: To learn how banks function and why economic downturns can threaten financial institutions.

Materials: Index cards, play money, calculators, chart paper.

Instructions:

Divide students into groups representing banks, businesses, farmers, and consumers.

Banks collect deposits and issue loans.

Run several rounds representing economic prosperity.

Introduce challenges such as falling crop prices, business failures, and unpaid loans.

Track how these events affect each bank's finances.

Discuss why some banks survive while others fail.

Learning Outcome: Students will understand the interconnected nature of banks, businesses, and consumers in the economy.

Investigating the Causes of Bank Failures

Recommended Age: 13–18

Activity Description: Students become historical investigators examining why a fictional bank failed during the Great Depression.

Objective: To identify and analyze the major causes of bank failures between 1929 and 1933.

Materials: Case-study packet, evidence cards, worksheets.

Instructions:

Provide students with evidence cards describing risky loans, declining farm prices, stock market losses, and depositor panic.

Students work in teams to determine which factors caused the bank's collapse.

Each team presents its findings.

Compare conclusions and discuss how multiple factors often combined to create failures.

Learning Outcome: Students will understand that bank failures resulted from a combination of economic weaknesses, poor decisions, and public panic rather than a single cause.

Comments